Think About It..

According to one source, California has $1.5 TRILLION in unfunded pension liability. “Unfunded pension liability” represents that portion of the state’s pension obligation not covered by agency and employee contributions. Another way of putting it is this: “in order to keep paying your pensions, we need to come up with about $1.5 trillion dollars, but we don’t know where we’re going to get it.”

There are 39.2 million citizens in California and that means that each man, woman, and child is potentially on the hook for about $38,200 dollars. You have a family of four? You owe us $152,900, give or take a few hundred.

Meanwhile, have you noticed how run down things are getting in California? The potholes that are not getting filled? The community parks that are full of weeds? The graffiti covered traffic signs that are not being replaced? On a trip to Tennessee a few years back, I noticed that the public schools looked brand new, the roads were re-surfaced, and parks were pristine. Guess what? Tennessee unfunded pension liability, per person, amounts to about $488. Think about that: $38,200 per person in California and $488 per person in Tennessee.

Here’s how it works. If a city or a school district has to make a larger and larger pension contribution payment each month, what gives? You pay your staff (active and retired) first and everything else afterwards. If there’s not enough left over for new paint, or remodeled restrooms or new traffic signals, well, things just get more and more shabby–and dangerous. The City of San Jose, with one of the worst unfunded pension liability burdens in the state, has to choose between paying retired workers or providing necessary services.

There is no easy choice here. If you keep reducing services, in order to pay retirees, the absurd, final result would be a community that pays taxes SOLELY for the purpose of paying retired employees. “Sorry, we have no water utilities, no trash disposal, no police or fire. You just pay your taxes to keep retirees on the golf course.” On the other hand, try handing a $152,000 invoice to every California family. See what happens. Something has to break and everyone knows it. Not even the Democrats are brave enough to ask the taxpayers to fully fund pensions they knew would never work in the first place. (It’s time to start voting for adults, people.)

When someone can put 30 years in with a public agency, retire at fifty, and live handsomely off the taxpayers until they are 75 to 90, it sounds wonderful, doesn’t it? Unfortunately, somebody has to pay for it. The retiree’s work time contributions don’t come close to covering it, obviously. That’s what we mean by “unfunded.”

The gross unfairness of these public pensions is made obvious in a conversation that would seem surreal, if it took place in the private sector.

Worker: I want to set up a pension that pays me 90% of my final salary when I retire, and maybe even add in another 20% if I have a disability. Oh, and throw in cost of living adjustments.

Financial Consultant: I’m afraid the definitions are too vague there. How many years do you plan on working? How long will you live after you retire? What will your final salary be? How do we account for fluctuations in investment return?

Worker: Well, can’t we just create some unfunded liability account and let somebody else pay for it?

Financial Consultant: Pardon? What did you say?

This is really a forbidden topic because lots of civil servants just assume this fantasy land will go on forever, and lots of private sector workers are worried they will have to pay for that fantasy retirement, even though they will never enjoy anything close to that themselves.

Why hang on, Grandpa?

Maybe the whole problem would go away, or be reduced, if… dare we think it?

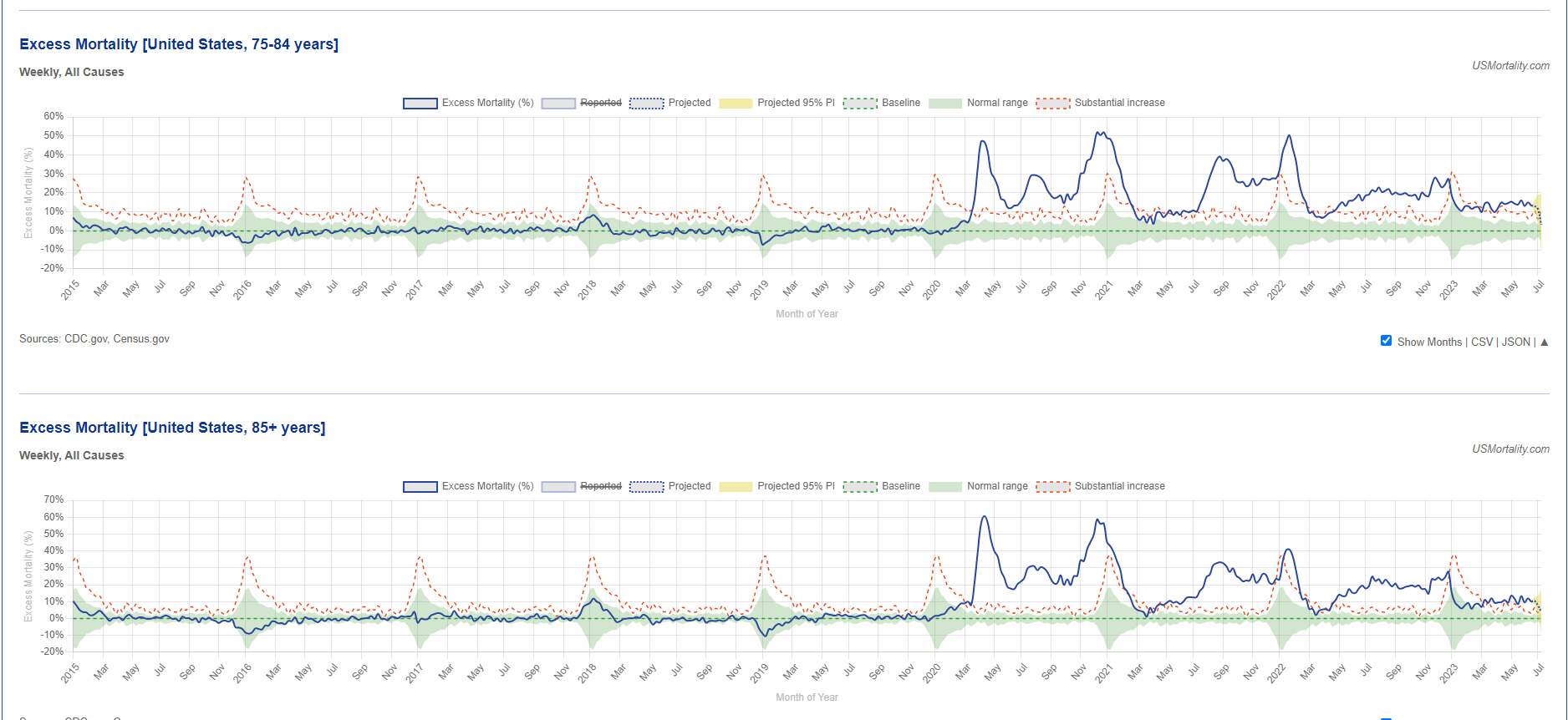

Hear me out on this: none of the legacy media pays much attention to it, but ever since March of 2020, “excess mortality” has drastically increased. By “increase,” we don’t mean a little upward blip. Some folks believe we are above the averages by several standard deviations. Depending on who does the math, we’re talking about increases in mortality that would only happen every 700 years. A LOT more people are dying, particularly older people.

Take a look. (Source)

Sovereign debt (the debt owed by governments around the world) is mushrooming, and a lot of it has to do with the commitments we have made to an aging population, particularly that portion of the population enjoying a civil service pension.

Put these realities together..

- We promised all these people lifetime pensions

- Those people are living longer

- We’re having trouble making payments

Given that we now know beyond all reasonable doubt the Commie virus was developed in a Commie lab, using money from US taxpayers, are you telling me there aren’t soul-dead, bloodless elites who are capable of doing this sort of dark math? Even Australia is now beginning to question the safety of mRNA vaccines. The displacement created by lockdowns, business failures, depression are certainly taking a toll. SOMETHING is making grandma and grandpa die sooner, and in larger numbers.

Are we witnessing a hideous, global genocide supervised by people who need to reduce sovereign debt? Is it outlandish to think the very same sort of people who shamelessly promised unsustainable pensions would consider shaving away some of the old folks, to reduce the burden, or kick the can down the road? Picture a global policy type, somewhere in dark orbit of Klaus Schwab, gleefully cheering on double jabs for grandma every year — and then celebrating a downturn in pension obligations.

Remember, extermination camps and gulags are so 1943. Isn’t there a neat and tidy, modern, way of doing this?

Who knows?

But it wouldn’t surprise me. Not in the least.